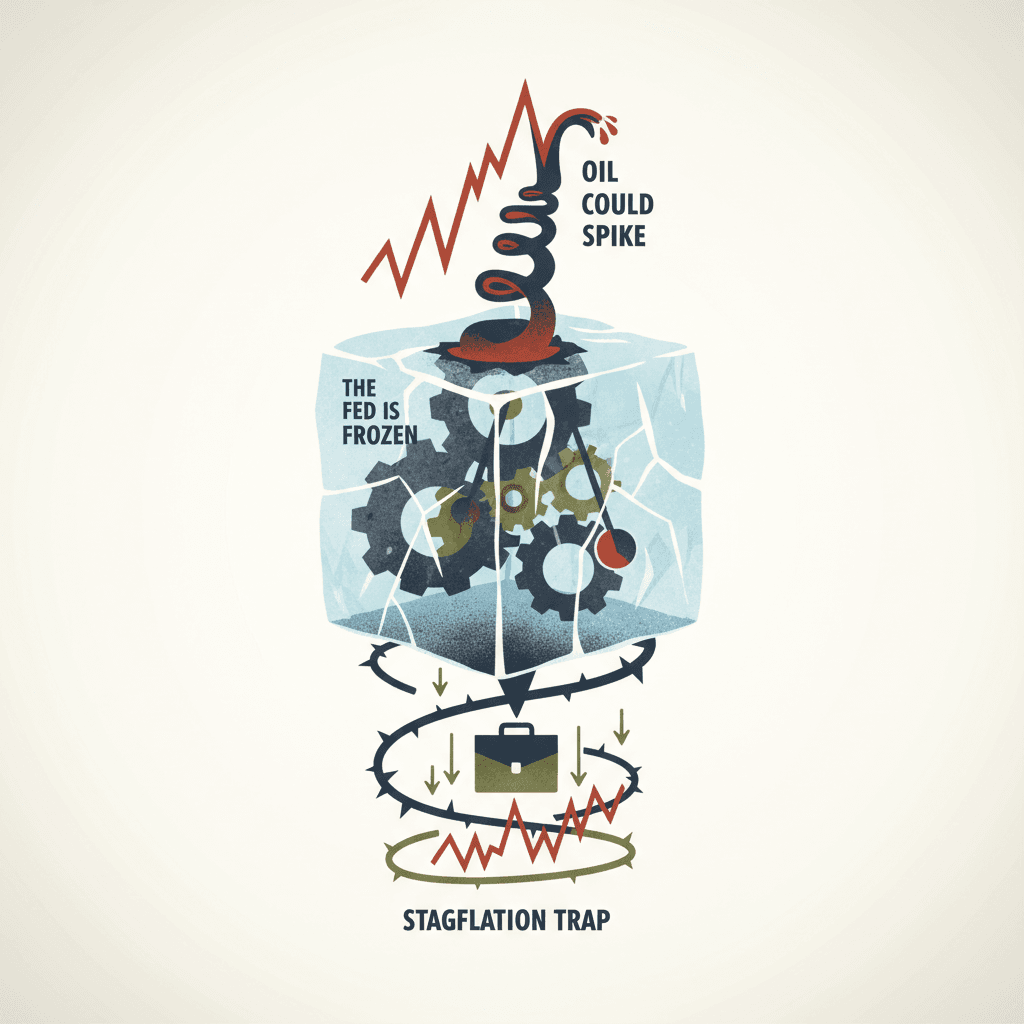

The Fed Is Frozen, Oil Could Spike, and the Economy Is Slowing. That's the Stagflation Trap.

Imagine you're driving and your engine starts overheating while the temperature outside drops below freezing. You can't turn the heater off without freezing, and you can't keep it on without blowing the engine. That's roughly where the Federal Reserve finds itself right now, and prediction markets are putting hard numbers on just how stuck they are.

The Numbers That Tell the Story

Prediction markets are pricing in a 98.5% probability that the Fed does absolutely nothing at its April 2026 meeting. Not a rate hike, not a rate cut, nothing. The chance of even a modest 25 basis point cut (a quarter of a percentage point reduction in the benchmark interest rate) sits at just 1.5%. A hike of any size? 0.5%. The Fed isn't just cautious. It's paralyzed.

And this isn't expected to change anytime soon. Looking at the full year, there's a 40.5% chance the Fed makes zero rate cuts in all of 2026. Even the June meeting only shows a 6.5% chance of a 25 basis point cut. The federal funds rate, which is the interest rate banks charge each other overnight and the lever the Fed pulls to steer the economy, looks locked at its current range.

Meanwhile, the economy is flashing warning signs. Prediction markets put the probability of a recession in 2026 at 29.5%. There's a 36.5% chance that unemployment climbs above 5% before 2027. Those aren't panic-level numbers, but they're high enough that the Fed would normally be thinking about cutting rates to stimulate growth.

So why won't they? Because of the other side of the equation: inflation pressure from energy costs. Betting markets show a 56% chance that WTI crude oil (the benchmark price for U.S. oil) hits $140 or higher by year-end. There's a 40% chance it reaches $150 to $160, and even a 24.5% chance it touches $180. With oil currently trading around $60-65, those are staggering moves that would send gasoline and shipping costs through the roof.

This is the self-reinforcing loop that makes stagflation so dangerous:

- Oil prices spike, raising costs for businesses and consumers across the economy.

- Higher costs slow economic growth and push unemployment up.

- The Fed would normally cut rates to fight the slowdown, but can't because cutting rates would pour gasoline on the inflation fire.

- The Fed would normally raise rates to fight inflation, but can't because raising rates would crush an already weakening economy.

- The paralysis continues, and both problems get worse.

Ray Dalio, the founder of Bridgewater Associates, has warned about exactly this kind of trap for years. He calls it a breakdown in the "economic machine," where the central bank's two jobs, keeping prices stable and keeping people employed, become impossible to do at the same time.

What This Means for Markets

The combination of a frozen Fed, rising recession risk, and potential oil price shocks creates a toxic environment for most traditional investments. The S&P 500 has only a 48% chance of finishing above 6845 by year-end, which is essentially a coin flip on whether stocks go up or down. The Nasdaq faces a 17% chance of dropping below 19,000. Long-duration bonds, the kind of bonds that pay out over 10 or 20 years, get hit from both directions: inflation fears push yields up while economic weakness prevents the safe-haven rally that bonds usually enjoy during slowdowns.

This is a wide distribution of outcomes, and the tail risk (the chance of something really bad happening) is meaningfully skewed to the downside.

Selling Shovels in a Stagflation Gold Rush

During the California Gold Rush, the people who made the most reliable money weren't the miners. They were the folks selling pickaxes, shovels, and blue jeans. The same logic applies when navigating a stagflation environment: instead of betting on one specific outcome, you look for the assets that profit from the broader trend regardless of which exact scenario plays out.

Gold is the ultimate shovel here. GLD, the SPDR Gold Trust ETF, gets a BUY signal at 75% confidence, the highest conviction call in this pattern. Gold benefits from every branch of the stagflation tree. Inflation stays elevated because of oil? Gold goes up. Economic uncertainty rises from recession risk? Gold goes up. The Fed stays frozen and real interest rates (the rate after subtracting inflation) get compressed? Gold goes up. Geopolitical tensions around Iran drive the oil spike? Gold goes up. It profits from the entire trend of monetary policy confusion, not just one piece of it.

Energy stocks are the other major shovel play. XLE, the Energy Select Sector SPDR Fund, earns a BUY signal at 68% confidence. XLE holds the big integrated oil companies like Exxon and Chevron that benefit from elevated oil prices. Unlike buying oil directly through a fund, energy stocks don't suffer from contango decay (a structural cost where futures contracts lose value as they roll forward month to month). These companies also generate real cash flows and serve as natural inflation hedges because their revenues rise with the prices that are causing the inflation.

HAL, Halliburton, is the classic shovel-seller within the oil industry itself. It gets a BUY signal at 65% confidence. Halliburton provides the completion and production services that every oil producer needs, regardless of which specific drilling company wins. In a high-price environment with supply constraints (prediction markets show a 58% chance that no Iran nuclear deal floods the market with supply), there's enormous pressure to maximize output from existing wells, and that's Halliburton's bread and butter. They benefit from activity levels, not just commodity prices.

On the defensive side, SH, the ProShares Short S&P 500 ETF, gets a BUY signal at 62% confidence as a direct hedge against broad equity declines. With the Fed unable to ride to the rescue, a 29% recession probability, and oil-driven margin compression squeezing corporate profits, this is the most straightforward way to position for equity downside.

USO, the United States Oil Fund, only gets a WEAK BUY at 50% confidence. While the oil spike probabilities look compelling on paper, the 24-hour changes in those prediction market contracts show significant bearish movement (down 5.3% to 13.3%), suggesting the market is already repricing those odds lower. The contango decay problem with USO's fund structure also eats into long-term returns. This is a speculative tail-risk play at best.

TLT, the iShares 20+ Year Treasury Bond ETF, gets a NEUTRAL rating at 40% confidence. Long bonds are the textbook stagflation victim because they get damaged by both inflation expectations and economic weakness simultaneously. The frozen Fed means no rate cuts to push bond prices higher. But shorting bonds is also risky because if a recession does materialize, there would be a sharp flight-to-safety rally.

DBMF, the iMGP DBi Managed Futures Strategy ETF, earns a WEAK BUY at 55% confidence. Managed futures strategies, which use trend-following algorithms to go long or short across commodities, bonds, and currencies, have historically done well in stagflationary regimes because they can go long commodities and short bonds simultaneously. DBMF is the shovel for navigating regime uncertainty: it profits from trends in any direction rather than betting on one specific outcome.

Finally, VICI Properties, a real estate investment trust focused on casino and hospitality properties, gets a SELL signal at 65% confidence. REITs (companies that own income-producing real estate) are the direct victims of a frozen Fed. Their long-duration cash flows get discounted more heavily when interest rates stay higher for longer. The 40.5% probability of zero cuts in 2026 is especially painful for the REIT sector, which has been priced on the assumption that rate relief was coming. VICI is the "anti-shovel," the infrastructure that suffers regardless of which specific bad scenario unfolds.

The Risks You Need to Know

This analysis rests on several assumptions that could easily break down.

The recession probability is 29%, which means there's a 71% chance no recession happens. If the economy powers through with stronger-than-expected growth, the stagflation thesis loses a leg and equities could rally significantly. Markets have a persistent upward bias, and betting against stocks has a long history of losing money over time.

The oil spike probabilities look dramatic, but they're already moving against the thesis. The 24-hour changes in oil prediction markets show prices dropping 5% to 13%. If an Iran nuclear deal comes through (prediction markets show a 42% probability), that would flood the market with supply and crush energy prices. And there's a fundamental tension in the data itself: it's hard to have $140+ oil and a recession at the same time, because the recession would destroy enough demand to bring oil prices back down.

Gold is already near all-time highs, limiting the asymmetric upside that makes for the best trades. A strong dollar, which high interest rates tend to produce, is historically a headwind for gold. And if a liquidity crunch materializes alongside a recession, even gold can sell off as investors scramble for cash.

Inverse ETFs like SH suffer from daily rebalancing decay in choppy or sideways markets. If the market grinds sideways for months rather than making a decisive move down, SH will slowly bleed value. Shorting REITs like VICI is already a crowded trade, and VICI's triple-net lease structure (where tenants pay all operating expenses) provides very stable cash flows that may hold up better than the stock price suggests. The dividend yield also creates a natural floor.

For energy stocks, the ESG-driven structural selling pressure hasn't gone away, and if the oil spike is driven by geopolitical supply disruptions rather than demand, U.S. producers may not benefit as much as OPEC nations. Halliburton faces the risk that North American shale operators maintain capital discipline even at high prices, choosing to return cash to shareholders rather than drill more wells.

Why This Matters for Your Money

If you have a 401(k) or any retirement savings in a standard target-date fund, you're probably holding a mix of stocks and bonds. Stagflation is the one environment where both of those can lose money at the same time. Your stock holdings get hurt by the economic slowdown, and your bond holdings get hurt by persistent inflation. Understanding this dynamic helps you think about whether some allocation to real assets like commodities or gold might make sense as insurance.

On a more everyday level, if oil really does spike toward $140 or higher, you'll feel it at the gas pump, at the grocery store (because shipping costs rise), and in your heating bills. The fact that the Fed can't cut rates to help means mortgage rates stay elevated too, keeping the housing market frozen for buyers. And the 36.5% chance of unemployment climbing above 5% means the job market could get noticeably tighter in certain sectors.

None of this is guaranteed to happen. But the prediction markets are telling us the probability distribution is unusually wide and unusually dangerous, with over $15.3 million in volume across these contracts. When the central bank can't do its job because its two mandates are pulling in opposite directions, the range of possible outcomes gets much wider than normal. Planning for that uncertainty, rather than assuming everything will be fine, is the smart move.

Analysis based on prediction market data as of April 6, 2026. This is not investment advice.

How This Story Evolved

First detected Mar 20 · Updated daily

The headline was updated to highlight prediction markets as the source for stagflation concerns, replacing the mention of a slowing economy. The article's body made mostly small wording tweaks, like changing "serious" to "significant" and updating a subheading, but the overall meaning stayed the same.

Read latest →The headline was slightly reworded to make it flow more naturally, but the meaning stayed the same. The opening analogy changed from a car with stuck pedals to one with an overheating engine and failing brakes, and the article now more directly mentions the impact on personal portfolios.

Read this version →The article's opening was rewritten to start with a car analogy to make the Fed's situation easier to picture, before getting into the prediction market data. The new version also jumps more quickly into specific numbers, like the 98% probability of no Fed action, while the old version eased into the topic more gradually.

Read this version →The new version removed the car overheating analogy that opened the article and jumped straight into explaining the situation. It also added a clearer, simpler definition of stagflation early on for readers who may not know the term.

Read this version →The stagflation story stayed largely the same, but the focus sharpened — concerns about a slowing economy were dropped from the headline, leaving oil prices and the Fed's inability to act as the main worries. Investors appear to be moving toward energy and short-term safe assets while pulling back from longer-term bonds and some previous energy plays.

Read this version →The article updated its car analogy to better illustrate a "stagflation trap," where both action and inaction cause harm. The headline and framing now explicitly highlight a slowing economy alongside the frozen Fed and oil threat, painting a more complete picture of stagflation risks.

The article updated its car analogy from a stuck gas pedal and brake to one where both pedals cause damage, making the Fed's situation sound even more dangerous. The headline also changed to more directly warn readers about the impact on their portfolio.

Read this version →The article swapped out the overheating car analogy for a locked steering wheel analogy to describe the Fed's situation. The section header also changed from "The Fed Can't Move" to "A Central Bank With Its Hands Tied," but the core message and statistics stayed the same.

Read this version →